大成研究

全球资源 本土智慧

随着跨境投资日益频繁,外商从中国境内企业取得股息、红利等权益性投资收益的税务处理,已成为跨境架构设计与资金汇出管理中的核心事项。

此类所得属于来源于中国境内的应税所得,我国税法对其征收规则、扣缴义务、协定优惠及适用条件均有明确规范。实务中,税率和税收优惠的适用等,直接影响境外投资者的实际税负与资金回流效率。

本文将结合现行税收法律规定、税收协定及征管口径,就外商取得境内股息红利的涉税规则与税收优惠适用性进行分析和梳理。

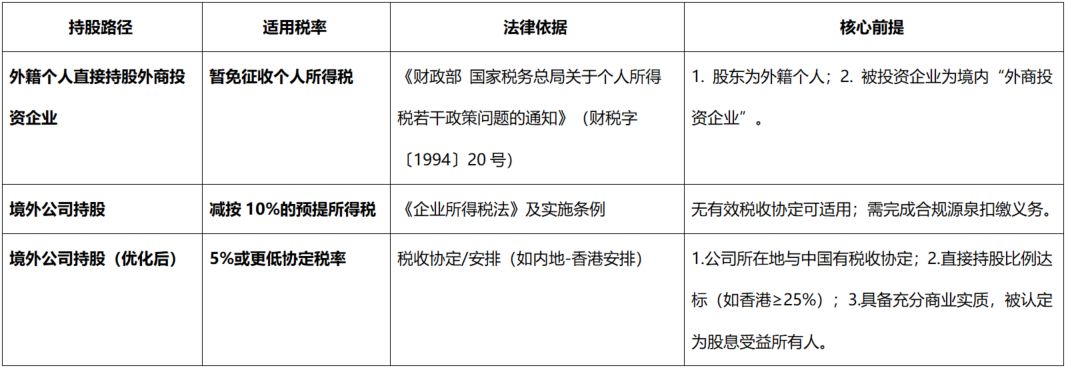

外商取得来源于中国境内的股息、红利等权益性投资收益时,需要向中国政府缴纳税款,而支付股息的企业是法定扣缴义务人,也就是说,境内企业向境外股东支付股息红利分配前,需要先扣掉税款。

然而,境内企业的外商股东所在地及性质决定了税款缴纳的多少。若股东为境外企业,则需根据该企业(或该企业的受益所有人股东)所在国或所在地与中国政府是否有更优惠的税收协定来确认税率;但若股东为外籍个人,则有可能享受免税待遇。

若以境外法人作为公司股东投资中国境内,则分红税款的优惠税率为10%,此为《企业所得税法》及《企业所得税法实施条例》规定的预提所得税优惠税率,相应税款应在实际支付(汇出)或者到期应支付(汇出)之日起7日内向主管税务机关申报和解缴代扣税款。

若境外企业股东所在地区(或国家)与中国签有税收协定(如内地与香港的安排),且该股东能证明其是股息的“受益所有人”,则可申请享受更低税率(例如5%)。

享受优惠税率时,非居民纳税人(境外股东)应“自行判断、申报享受、相关资料留存备查” ;境内支付企业作为扣缴义务人,也需留存非居民纳税人提交的《非居民纳税人享受协定待遇信息报告表》,并按其申报的协定待遇扣缴税款。

需要注意的是,受益所有人身份的判定对享受税收协定待遇具有决定性意义,根据《国家税务总局关于税收协定中“受益所有人”有关问题的公告》(国家税务总局公告2018年第9号),受益所有人是对所得或所得据以产生的权利或财产具有所有权和支配权的人。针对境外企业取得中国境内股息所得申请享受税收协定优惠的情形,即便直接持股的收款方不符合股息 “受益所有人” 判定条件,在满足法定穿透规则的前提下,仍可依据符合“受益所有人”身份的中间层或最终控股股东,申报享受对应税收协定(安排)的优惠税率。需要注意的是,相关境外主体具备真实的实质性经营活动,是判定“受益所有人”身份、享受协定优惠待遇的核心前提。

若境外股东为个人,在符合一定条件的前提下,境内分红可免税汇出。根据《财政部 国家税务总局关于个人所得税若干政策问题的通知》(财税字〔1994〕20号),外籍个人从我国外商投资企业取得的股息、红利所得,可暂免征收个人所得税。

该政策旨在优化营商环境,吸引海外人才与投资。要想适用外籍个人免税政策,需同时满足“投资者为外籍个人”与“境内企业为外商投资企业”双重条件。

需要注意的是,2013年《国务院批转发展改革委等部门关于深化收入分配制度改革若干意见的通知》(国发〔2013〕6号)曾提出“取消对外籍个人从外商投资企业取得的股息、红利所得免征个人所得税等税收优惠”。

但在税收征管实务中,该文件被视为一项宏观工作部署,其具体落实有待财政、税务部门出台明确的废止文件或替代政策。与此同时,《财政部 税务总局关于继续有效的个人所得税优惠政策目录的公告》(财政部 税务总局公告2018年第177号),已明确将财税字〔1994〕20 号文纳入继续有效的优惠政策目录,由此可见,该文件仍是有效的执法依据。尽管如此,极少数地方税务机关在个案中可能存在不同理解,建议企业在实际操作前聘请专业顾问与主管税务机关进行确认。

从税务成本角度进行理论推演,一种可能的优化路径是:在符合法律法规的前提下,直接由符合条件的外籍个人持股,可享受股息红利个人所得税暂免征收的待遇;若采用公司架构,则可考虑在与中国签有优惠税收协定(如内地与香港的安排)且具备商业实质的辖区设立中间控股公司,以期适用更低的协定税率。必须强调的是,任何投资架构的设计都必须以真实的商业目的、充足的商业实质和经济实质为基础,严格遵守反避税规则(如国家税务总局公告2015年第7号)及国家税务总局公告2018年第9号“受益所有人”管理的规定,并综合考虑法律责任、控制权、未来退出等多重非税因素。在进行具体架构设计前,务必咨询专业的税务及法律顾问。

需要注意的是,对于无实际经营业务、仅为资金跨境调度设立的空壳外商投资企业,税务机关有权依据实质课税原则,否定其外籍个人股息红利免税优惠的适用资格;通过不合理定价、虚构业务转移利润的,将面临反避税调查与纳税调整。

外商投资者需确保外商投资企业具备真实的商业实质,拥有与经营规模相匹配的人员、资产与业务体系,关联交易严格遵循独立交易原则,杜绝无商业目的的空壳化运营与激进税务筹划,确保税收优惠政策的合法适用。

综上,外商投资境内企业在股息红利分配环节的税务处理,兼具法定性、协定适用性与实质审查性。无论是企业股东适用协定优惠税率,还是外籍个人享受暂免征税待遇,均需建立在真实交易、合理商业目的与充分实质经营的基础之上,避免因架构空洞、缺乏实质而被税务机关否定协定待遇或启动反避税调整。

外商在搭建境外持股架构、规划利润汇出路径时,应统筹税务成本、法律合规、资金安全与长期退出安排,在合法合规的前提下实现税负最优与风险可控。

How Foreign Nationals and Immigrant Families Can Invest in China and Enjoy Tax Benefits

With the increasing frequency of cross-border investments, the tax treatment of dividends and other equity investment income derived by foreign investors from Chinese domestic enterprises has become a core issue in cross-border structuring and capital repatriation.

Such income is classified as China-sourced taxable income. China’s tax laws provide clear rules on taxation, withholding obligations, treaty benefits, and the applicable conditions. In practice, the applicable tax rate and availability of tax incentives directly impact the effective tax burden of overseas investors and the efficiency of capital repatriation.

This article analyzes and outlines the tax rules and applicability of tax incentives concerning dividends derived from China by foreign investors, based on current tax laws, tax treaties, and prevailing tax administration practices.

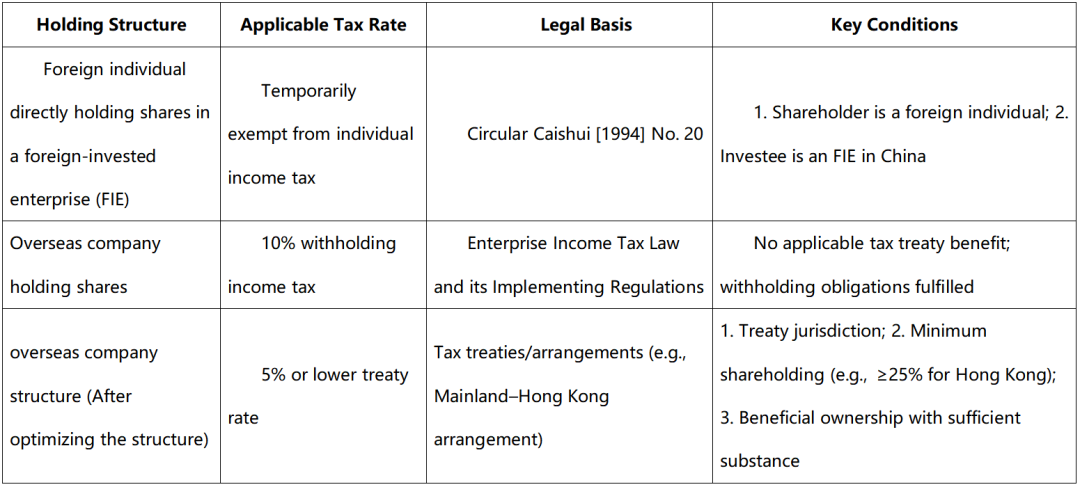

When foreign investors receive dividends or other equity investment income sourced from China, taxes must be paid to the Chinese government. The distributing enterprise acts as the statutory withholding agent. In other words, before distributing dividends to overseas shareholders, the domestic company must withhold the applicable taxes.

However, the amount of tax payable depends on the location and nature of the foreign shareholder:

i.If the shareholder is an overseas enterprise, the applicable tax rate depends on whether a tax treaty exists between China and the jurisdiction of the shareholder (or its beneficial owner), and whether a preferential treaty rate can be applied.

ii.If the shareholder is a foreign individual, tax exemption may be available under certain conditions.

If a foreign corporate entity invests in a Chinese company, dividends are generally subject to a 10% withholding income tax, as stipulated under the Enterprise Income Tax Law and its implementing regulations. The tax must be declared and paid to the competent tax authority within 7 days from the date the payment is made or becomes payable.

Where the jurisdiction of the overseas shareholder has a tax treaty with China (e.g., the Mainland–Hong Kong arrangement), and the shareholder qualifies as the beneficial owner,a reduced tax rate (e.g., 5%) may apply.

When claiming preferential tax rates, the non-resident taxpayer (i.e., the overseas shareholder) shall self-assess eligibility, claim the treaty benefits accordingly, and retain relevant supporting documents for future inspection. The domestic paying enterprise, acting as the withholding agent, is also required to retain the “Information Reporting Form for Non-Resident Taxpayers Claiming Treaty Benefits” submitted by the non-resident taxpayer, and withhold tax in accordance with the treaty benefits as claimed.

It is important to note that beneficial ownership is crucial in determining eligibility for treaty benefits. According to SAT Announcement [2018] No. 9, a beneficial owner is a person who has ownership and control over the income or the rights/assets generating such income.

In cases where a non-resident enterprise derives dividend income from China and seeks to apply treaty benefits, even if the immediate recipient (i.e. the direct shareholder) does not meet the criteria for being the “beneficial owner” of such dividends, preferential tax treaty rates may still be claimed, provided that the statutory look-through rules are satisfied, by reference to an intermediate or ultimate controlling shareholder that qualifies as the “beneficial owner” under the relevant tax treaty (or arrangement). However, having substantive business activities is a key legal requirement for recognition as a beneficial owner.

If the shareholder is a foreign individual, dividends distributed from China may be exempt from individual income tax, subject to certain conditions. According to Circular Caishui [1994] No. 20, dividends and bonuses received by foreign individuals from foreign-invested enterprises in China are temporarily exempt from individual income tax.

This policy aims to improve the business environment and attract foreign talent and investment. To qualify, both conditions must be met: i. The investor is a foreign individual; ii. The investee is a foreign-invested enterprise in China.

It should be noted that in 2013, a State Council document (Guofa [2013] No. 6) proposed abolishing such tax exemptions. However, in practice, this document is regarded as a policy direction pending implementation.

Meanwhile, Announcement [2018] No. 177 issued by the Ministry of Finance and the State Taxation Administration confirmed that Circular Caishui [1994] No. 20 remains valid. Therefore, it is still an effective legal basis.

Notwithstanding the above, a few local tax authorities may adopt different interpretations in specific cases. It is advisable to consult professional advisors and confirm with the competent tax authority before implementation.

From a tax optimization perspective, one possible approach is: Provided that it complies with laws and regulations, direct investment by a qualified foreign individual, to benefit from dividend tax exemption; or use of an intermediate holding company in a treaty jurisdiction (e.g., Hong Kong) with sufficient commercial substance, to access reduced treaty rates. It must be emphasized that any investment structure must be based on: genuine commercial purposes; adequate business and economic substance; full compliance with anti-avoidance rules (e.g., SAT Announcement [2015] No. 7 and [2018] No. 9). Other factors such as legal liability, control rights, and exit strategies must also be considered. Professional tax and legal advice is strongly recommended before implementing any structure.

For foreign-invested enterprises that lack substantive operations and are established solely for cross-border fund transfers, tax authorities may apply the substance-over-form principle to deny tax exemption on dividends received by foreign individuals. Where profits are shifted through artificial arrangements or non-arm’s-length pricing, taxpayers may face anti-avoidance investigations and tax adjustments.

Foreign investors must ensure that their enterprises have: genuine business operations; personnel, assets, and operational scale commensurate with their activities; related-party transactions conducted in accordance with the arm’s length principle. Shell structures and aggressive tax planning without commercial purpose should be avoided to ensure lawful application of tax benefits.

The tax treatment of dividend distributions arising from foreign investment in domestic enterprises is characterized by statutory requirements, treaty applicability, and substantive review. Whether a corporate shareholder seeks to apply a preferential tax rate under an applicable tax treaty, or a foreign individual aims to benefit from a temporary tax exemption, such treatments must be grounded in genuine transactions, reasonable commercial purposes, and sufficient operational substance. This helps avoid the denial of treaty benefits or the initiation of anti-avoidance adjustments by tax authorities due to artificial structures or lack of substance.

When establishing offshore holding structures and planning profit repatriation routes, foreign investors should take a holistic approach that balances tax efficiency, legal compliance, capital security, and long-term exit strategies, so as to achieve optimal tax outcomes while maintaining manageable risks within a compliant framework.

特别声明:

大成律师事务所严格遵守对客户的信息保护义务,本篇所涉客户项目内容均取自公开信息或取得客户同意。全文内容、观点仅供参考,不代表大成律师事务所任何立场,亦不应当被视为出具任何形式的法律意见或建议。如需转载或引用该文章的任何内容,请私信沟通授权事宜,并于转载时在文章开头处注明来源。未经授权,不得转载或使用该等文章中的任何内容。

本文作者

%%金融%% $$王旭$$

大成能为您做什么?

联系我们 +

Copyright ©2026 大成DACHENG 版权所有 | 保留所有权利 All Rights Reserved