大成研究

全球资源 本土智慧

本文主要描述当外籍人在持有美国投资期间去世时,所适用的美国联邦税务及相关程序。本文假设逝者并非美国公民或绿卡持有者,生前未在美国居住,且没有在美国定居的计划。

This article discusses the US federal taxes and procedures that apply when a foreign person dies while owning investments in the US. For this article, it is assumed that the decedent was not a US citizen or green card holder, they did not live in the US, and they did not plan to live in the US.

美国联邦政府征遗产税。部分州也征遗产税或继承税。但因50个州各自都有各自的法规,本文仅描述联邦遗产税。

The US federal government has an estate tax. Some, but not all, states have estate or inheritance taxes. But because each of 50 states has its own rules, this article only discusses the federal estate tax.

美国遗产税是对逝者的“遗产”征收的,因此遗产管理人有责任按时申报并缴税。如果遗产管理人能按规定申报并缴清美国遗产税,那么继承人就无需申报或缴继承税,且继承的财产也不被视为个人所得。但如果管理人未缴清遗产税,继承人就必须提交遗产税表。

The US estate tax is imposed on the decedent’s estate, and the administrator has obligation to ensure that the tax is filed and paid.[1] If the estate properly files and pays US estate tax, then the heirs do not need to file or pay an inheritance tax, nor is the inheritance considered income.[2] But if the administrator does not file and estate tax return, then heirs who inherit property must file estate tax returns.[3]

美国遗产税分别针对两类人群:1. 美国公民和居民;2. 非居民非公民。

在遗产税下,“美国居民”指的是在美国定居(domiciled)的人。遗产税对“居民”的定义与所得税定义不同。一个人只有当他在某个地方居住,并且没有离开该地的意图时,才在该地“定居”。每个案子需要分析实际情况,而绿卡仅是考量因素之一。

本文假设逝者既不是美国公民,也没有持有绿卡;生前不在美国居住,也没有计划去美国居住,且客观情况也能佐证其主观意图。因此,根据遗产税规定,他属于“非居民非公民”。

US estate tax differs between 1. US citizens and residents and 2. Nonresident noncitizens.

In the estate tax context, a US resident is a person who is domiciled in the US.[4] The estate tax definition is definition from a US resident in the income tax context.[5] A person acquires a domicile by living in a place with no intention of moving from there.[6] It is a highly fact-specific analysis, of which a green card is merely one factor.[7]

This article assumes that the decedent was not a US citizen or green card holder, they did not live in the US, they did not plan to live in the US, and objective circumstance support their intentions. Therefore, they were nonresident noncitizens under estate tax rules.

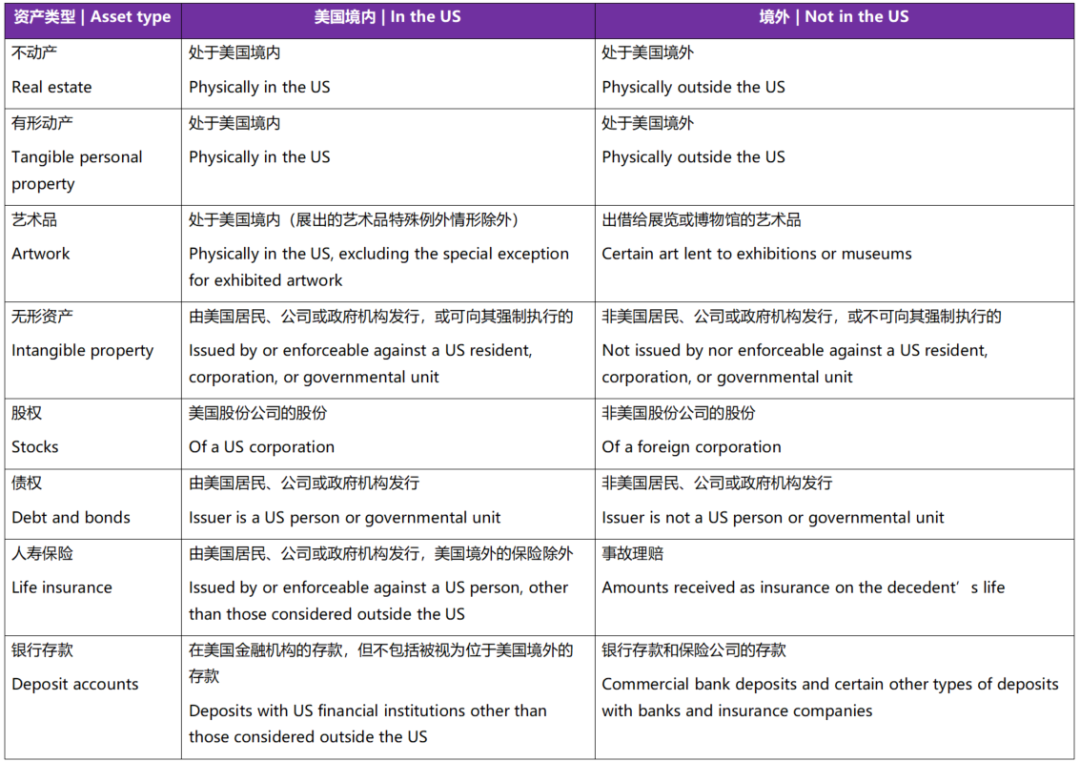

美国会对非居民非公民的美国境内资产(US situs assets)征遗产税。以下将分别列举属于美国境内和境外的资产类型。

The US taxes nonresident noncitizens on their assets in the US (US situs assets).[8] The following are assets in the US and outside the US.[9]

强调几条资产所在地的规则。

股票的所在地等于公司注册地。股票交易所的所在地和经纪账户的所在地没有影响。美国存托凭证(ADRs)是由美国券商发行的外国公司股票所有权凭证,但ADR属于境外资产。目前IRS并没有针对存放在外国券商处的美国股票是否适用对等规则的明确指引。

非居民非公民在美国银行存款账户免征美国遗产税。但保险箱里的现金(即使是在银行的保险箱)和在其他美国金融机构的现金账户,属美国境内遗产。

目前对加密货币的所在地无特别税务裁决。加密货币属于无形资产,但目前尚不明确它可以向谁主张权利。一种可能性是,如果首次代币发行(ICO)的发起人是美国人,或者该区块链是美国人管理,那么该加密货币就可能被视为可向美国人主张权利,从而被认定为美国境内资产。

Several of these location rules are worth highlighting.

The location of stocks is based on the corporation’s place of incorporation. The location of the exchange and the location of the brokerage account do not matter. American Depository Receipts (ADRs) are certificates of ownerships of stocks of foreign corporations issued by US brokerages, but ADRs are foreign situs assets.[10] There is no symmetric guidance for shares of US stocks held at foreign brokerages in general.

A nonresident noncitizen’s commercial bank deposit accounts at a US bank are exempt from US estate tax. Cash stashed in safe deposit boxes (even at commercial banks) and cash accounts with other US entities are US situs assets subject to US estate tax.

There have not been any rulings on the situs of cryptocurrencies. Cryptocurrency is intangible property, but it is not clear who it is enforceable against. It is possible that if the ICO sponsor is a US person, or the blockchain has a manager who is a US person, then the cryptocurrency is enforceable against a US person and considered US situs assets.

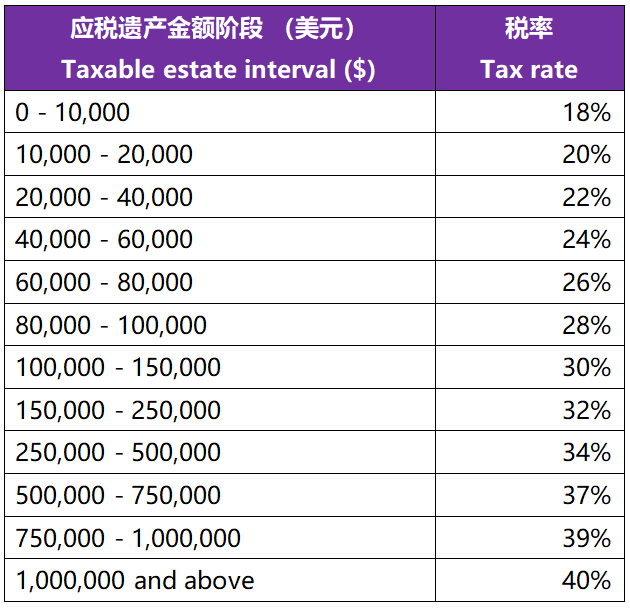

遗产税率按应税遗产金额计算。

US estate tax is imposed on the taxable estate at the following rates[11]:

遗产税的税率不受通货膨胀率影响。

Unlike the income tax brackets, the estate tax brackets are not adjusted for inflation.

计算应税遗产额,要从总遗产额中扣除以下各项:费用、债务、损失、税款、慈善捐赠以及配偶扣除额。其中,费用、债务、损失和税款需按全球遗产总额的比例进行分摊。

To calculate the taxable estate, subtract the following from the gross estate: Expenses, debt, losses, taxes, charitable donations, and marital deduction.[12] Expenses, debt, losses, and taxes are apportioned to the worldwide estate.[13]

非公民非居民有13,000美元的抵免额,相当于前60,000美元应税遗产额给予免税。这两个金额均不随通货膨胀进行调整。

A noncitizen nonresident gets a credit of $13,000 to offset their US estate tax.[14] It corresponds to an exemption on the first $60,000 of taxable estate in the US. The amounts are not adjusted for inflation.

如果美国境内遗产超过60,000美元的免税额,遗产管理人必须提交Form 706-NA (非居民非公民的遗产税申报表)。

The executor must file Form 706-NA (estate tax return for nonresident noncitizens) if the gross estate in the US exceeds the exemption amount of $60,000.[15]

遗产税表在去世后的9个月内提交。管理人可以提交Form 4768,获得6个月的延期。美国境外的管理人也可以提交Form 4768申请额外的6个月延期,但申请第二次延期时,管理人必须说明无法在第一次延期期限前申报的原因。

The estate tax return is due 9 months after death.[16] The executor can file Form 4768 to get a 6-month extension of time to file.[17] It is possible for executors outside the US to file Form 4768 to get an additional 6 month extension, but the second extension requires the executor to explain why it was impossible or impractical to file within the first extended deadline.[18]

美国国税局(IRS)强制执行非居民非公民遗产税最常见的方式,是要求美国金融机构冻结逝者的账户,直到该机构收到IRS签发的转让证(transfer certificate)。这种执行方式可能对中国大陆居民带来问题,因为有可能大多数大陆外的资产在被冻结的账户里。因此,建议在其他地方预留足够的流动资金,以便缴纳美国遗产税。

The most common way for the IRS to enforce estate tax collection on nonresident noncitizens is to require US financial institutions to freeze the decedent’s account until the institution receives a transfer certificate. For Chinese mainland residents, the collections mechanism can be problematic, because the frozen accounts may be the only significant overseas assets they have. Thus, it is recommended to provide for sufficient liquidity to pay the US estate tax elsewhere.

美国国税局(IRS)可以签发转让证,解冻相关的金融账户。遗产管理人必须提交遗产税表,并缴美国遗产税或做出缴纳的安排。IRS不会在管理人交税表时自动签发该证明,因此管理人必须单独提出申请。

The IRS can issue a transfer certificate to the estate to unfreeze financial accounts. To obtain one, the estate must file an estate tax return and pay or make provisions to pay US estate taxes.[19] The IRS does not automatically issue the certificate when the estate files the estate return, so the estate must separately apply for one.

逝者的个人代表或遗产管理人必须提交逝者生前未申报的任何税表。逝者去世当年的个人所得税申报表涵盖1月1日至去世日,且必须在次年的4月15日之前申报。

The personal representative or administrator of the decedent must file any tax returns that the decedent had not filed.[20] For the year of death, the decedent’s personal income tax return covers January 1 to the date of death, and it is due by April 15 of the following year.[21]

常见资产在去世后继续产生收入。从去世之日起到遗产完全分配之日止,收入归属于遗产本身。遗产管理人必须交所得税表。

It is common that a decedent’s assets continue to generate income after death. From the date of death to the date the estate is fully distributed, the income belongs to the estate. The administrator of the estate must file income tax returns for the estate.[22]

◆遗产的所得税居住地

Tax residence of the estate

遗产的税务居住地与逝者并不一定相同。它适用“事实与情况”测试,其中包含诸多考量因素,例如逝者的国籍与定居地(domicile)、继承人的居住地、资产的所在地,以及遗产管理的执行地。

在美国进行的附属遗嘱认证(ancillary probate)有可能导致在所得税下外国遗产转变为美国遗产;而附属遗嘱认证的终结,则可能导致在所得税下美国遗产重新变回外国遗产。

The tax residence of the estate is not the same as the decedent. It’s a “facts and circumstances” test that includes many factors, such as the decedent’s citizenship and domicile, the residence of the heirs, the location of the assets, and where the estate is administered.[23]

It is possible for ancillary probate in the US to change a foreign estate into a US estate under tax rules and for the end of ancillary probate to change a US estate into a foreign estate.[24]

◆分配给继承人

Distributions to heirs

遗产需要为其收入缴纳所得税,但可以扣除分配给继承人的部分。尽管个人所得税率和遗产所得税率的最高税率均为37%,但遗产达到最高税率的应税所得比个人快得多。因此,如果继承人同意在协商本金分配的同时,先接收来自遗产的收入,这对自己是有利的。

An estate pays tax on its income, but it gets a deduction for distributions to heirs.[25] Although both individual tax rates and estate tax rates cap at 37%, estates reach the maximum tax rate at a much lower threshold than individuals.[26] Thus, it is in the interest of the heirs if they can agree to receive income from the estate, even while they are working out the division of principal.

“遗产(estate)”一词的定义因法律的不同而有差异。

在遗嘱认证法(probate law)下,遗产包括逝者名下、未通过其他法律机制(如共同所有权或信托)处置的资产。在所得税法下,遗产的定义与遗嘱认证法类似,但也有些例外情况,例如可以将可撤销信托(revocable trust)视为遗产的一部分。

而在遗产税法下,遗产则包括逝者生前拥有权益的财产。遗产税法的定义范围,可能会包括不属于遗嘱认证遗产的资产。它包括有生存者取得权(right of survivorship)的共有资产,这类资产会自动转移给共同所有人,而不会成为遗嘱认证遗产的一部分。它还可能包括以不可撤销信托(irrevocable trust)形式持有的资产,但前提是信托设立人保留了过多的控制权或受益权益。

当夫妻共同投资美国房地产时,常会出现一个问题。在许多州,除非地契(deed)另有规定,共同拥有房地产的夫妻是以带有生存者取得权的某种共有权形式持有的。一方去世后,在世的配偶自动继承整套房产。这可能导致该逝者的遗产中仅剩下一个金额不大的美国银行账户,而其他资产都在中国,并受外汇管控。

在这种情况下,美国国税局(IRS)可以向继承人征遗产税。此外,如果遗产管理人在向美国联邦政府缴税之前,先将付款给了其他人,那么该执行人将对欠联邦政府的税款差额承担个人责任,但责任限于其向他人支付的金额。

The word estate is defined differently, depending on the legal context.

Under probate law, the estate includes assets of the decedent that are not disposed of under other legal regimes, such as joint ownership or trusts. Under income tax law, the estate is similar to under probate law, with certain exceptions such as the ability to treat a revocable trust as part of the estate.[27]

Under estate tax law, the estate includes any property in which the decedent had an interest.[28] The estate tax definition can sweep in assets that are not part of the probate estate. It includes assets held under joint ownership with the right of survivorship, which automatically passes to the joint owner without becoming part of the probate estate.[29] It also may include assets held in irrevocable trust but over which the settlor retained too much control or beneficial interest in the trust.[30]

A common problem occurs when spouses invest in US real estate together. In many states, unless the deed specifies otherwise, state law says that spouses who own real estate together own it under some form of joint ownership with right of survivorship. Upon death, the surviving spouse automatically inherits the entire house. This may leave the estate with only a modest bank account in the US, with other assets in China and regulated by foreign currency control laws.

In such situations, the IRS can collect the estate tax from the transferee.[31] In addition, if the executor pays anyone other than the US federal government before the federal government, they are personally liable for the deficiency owed the federal government to the extent of the payments to others.[32]

为了处置美国境内财产,金融机构可能会要求遗产管理人向资产所在地的县(county)申请附属遗嘱认证。在所得税下,附属遗嘱认证可能会将外国遗产转变为美国遗产。因此,最好用架构隔离美国资产风险。

To dispose of property in the US, financial institutions may require the administrator to apply for ancillary probate in the county where the assets are located. The ancillary probate can change the estate from a foreign estate to a US estate for income tax purposes. It is best to limit the risk by firewalling US assets through a holding structure.

●注释:

特别声明:

大成律师事务所严格遵守对客户的信息保护义务,本篇所涉客户项目内容均取自公开信息或取得客户同意。全文内容、观点仅供参考,不代表大成律师事务所任何立场,亦不应当被视为出具任何形式的法律意见或建议。如需转载或引用该文章的任何内容,请私信沟通授权事宜,并于转载时在文章开头处注明来源。未经授权,不得转载或使用该等文章中的任何内容。

本文作者

大成能为您做什么?

联系我们 +

Copyright ©2026 大成DACHENG 版权所有 | 保留所有权利 All Rights Reserved